All too often, I receive emails asking about short-term trading strategies for extremely risky companies (see MedBox post below)... but what about blue-chip companies such as Intel? Earlier this year I advocated buying Intel stock for a few different reasons:

- It is one of the great technology companies that grew with the popularity of the personal computer, but has since been hurt by "The Death of the Personal Computer"-type statements from prominent investors and analysts

- The Windows XP OS, released in 2001 has been an extremely popular platform for personal users, universities, retail banks, government institutions, and ATM operators. This is due to its ease of use, security, and stability. However, security support for Windows XP ended this April. While most personal users and small/medium businesses have moved on to newer systems, about 90% of ATMs still use XP. As ATM operators begin to upgrade to newer software (mostly Windows 7), they will also need to upgrade their hardware to the 2010s-era, not the 2000s-era hardware they currently run on with XP. This is where Intel comes in. According to Retail Banking Research in London, there are approximately 200,000 ATMs in the United States that still use XP.

- Although many banks have started to make the shift towards newer Windows systems, many have elected to pay Microsoft to continue producing security updates (most contracts are for 1 year). In other words, the opportunity to ride the wave of hardware system updates is not over.

- Why Intel and not AMD or Microsoft? Microsoft, while a great company, derives only 10% of its revenue from the Windows Operating system. Most revenue comes from Microsoft Office and Windows Server. Simply put, you need a big % change in OS revenue to make a significant dent in the overall price of Intel stock. Furthermore, this news is most likely already built into the stock price. Why Intel over AMD? This comes down to company valuation and preference for ATM operators to go the Intel route. AMD is already trading at a P/E ratio of 89.38 with a 1y forward P/E estimate of 18.65. Intel's same numbers are 14.94 and 13.96, respectively. As you can see, investors aren't expecting much growth from Intel.

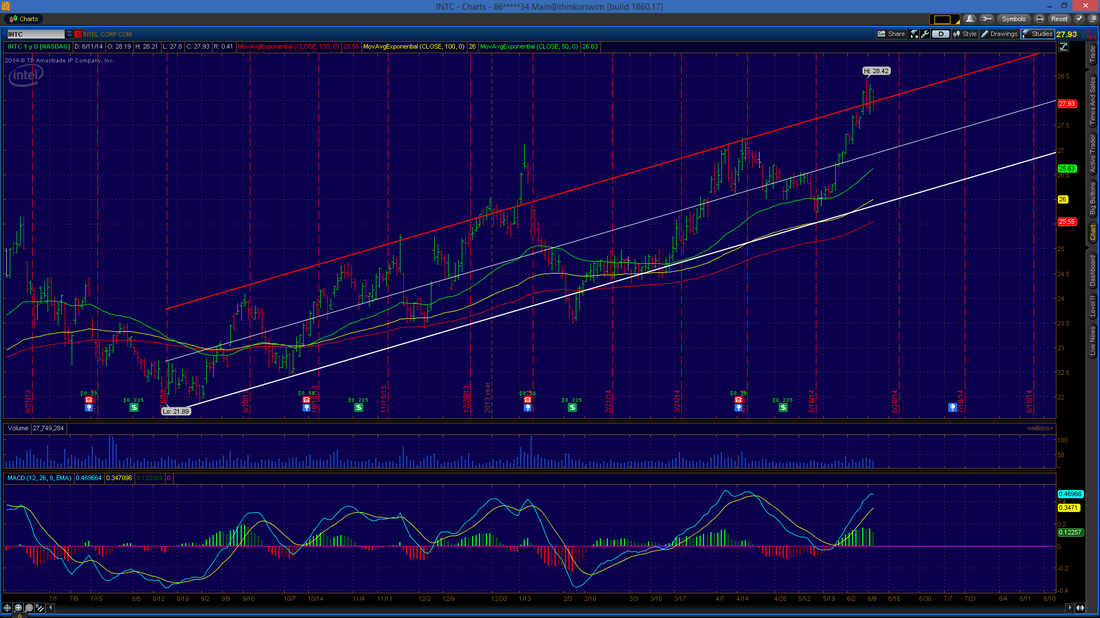

- It has been easy to trade since late last year. Barring regular company events such as dividend announcements and quarterly reports, Intel has been following a nearly perfect technical pattern since its 52-week low last August (see chart below). Traders who buy near the bottom of the regression channel and sell near the top will have made a significant profit. The regression channel runs from the August 2013 low to March 4th, 2014 (the first time I made the study) and haven't changed it yet.

CLICK TO ENLARGE IMAGE

6. While the trend described in (5.) will certainly not go on forever, traders should find comfort in knowing that Intel is a stable company and long-term prospects are encouraging.

So with a YTD return of over 8% versus less than 4% for the NASDAQ composite, is Intel still a great buy? Yes. With a low P/E ratio for the industry and reassuring growth prospects over the next 12- to 18-months, the price certainly doesn't match the potential. Oh, and for all of you dividend buffs out there, it pays a hefty 3.30% yield.

Trader's Thoughts

Start buying around $27, but save some cash for if and when it drops below $26.50.

So with a YTD return of over 8% versus less than 4% for the NASDAQ composite, is Intel still a great buy? Yes. With a low P/E ratio for the industry and reassuring growth prospects over the next 12- to 18-months, the price certainly doesn't match the potential. Oh, and for all of you dividend buffs out there, it pays a hefty 3.30% yield.

Trader's Thoughts

Start buying around $27, but save some cash for if and when it drops below $26.50.

RSS Feed

RSS Feed