"I'm thinking of making a big play on HollyFrontier Corporation before their Q3 2013 earnings report on November 6th. More than 5,700 November 48 call options were purchased on Friday, showing traders turning bullish on the company. What are your thoughts?"

HollyFrontier vs. Peers

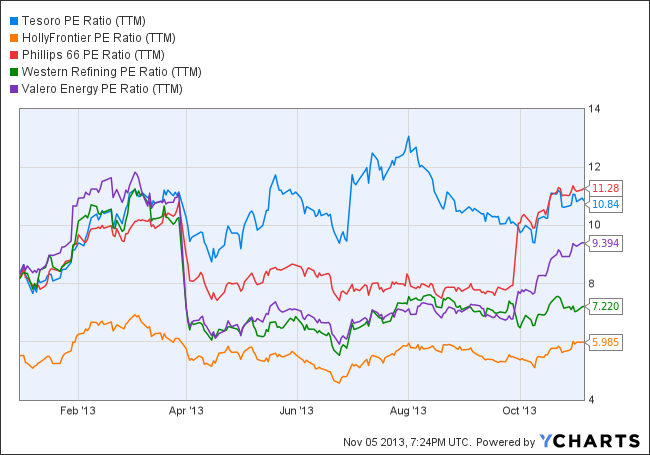

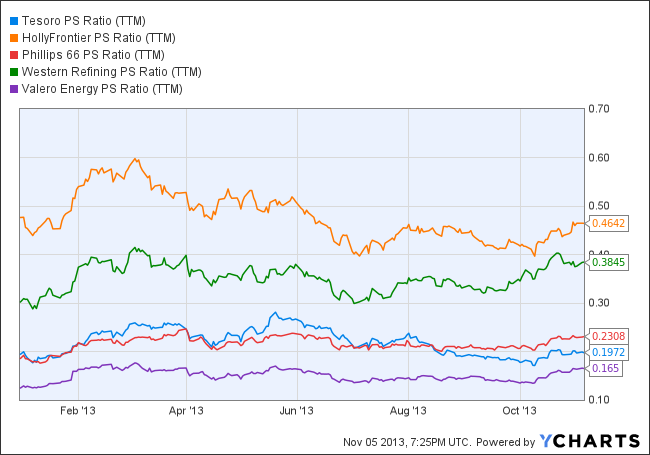

Two things I would like to point out before I get too in-depth with this analysis. First of all, one of the most important inputs in the profitability of oil refiners is the price of oil. As you can see from Figure 1, the price of oil during July 2013 to September 2013 (the quarter the company is reporting for) is the highest it has been all year. This is certainly a good sign for HollyFrontier, as its profitability has fallen behind its peers in recent quarters. Companies with shrinking margins tend to trade at higher price-to-sales ratios and lower price-to-earnings ratios than those of their peers. This is reflected in the PE ratio of oil refiners, where HollyFrontier has the lowest ratio versus its peers (showing an underpricing in the company’s stock – see Figure 2), and is also reflected in the PS ratio, where HollyFrontier has the highest PS ratio versus its peers (showing an overpricing in the company’s stock – see Figure 3). The downside to the company is that investors take into account the present value of all future cash flows when pricing a stock, and the price of crude oil has fell from over $110 per barrel in September to $93.39 today – not a good sign for the company’s bottom line for the 4Q2013 reporting.

Do Not Let Speculative Option Traders Deceive You

The second perspective that is important to mention is, historically, high option volume (whether it is puts or calls) does not indicate direction of a stock following its earnings report. Two recent examples were Apple, Inc.’s quarterly earnings released last week that were preceded by high call option volume. Before the report, the stock was trading at $529.88 versus $526.85 (keep in mind that the actual EPS of $8.26 was higher than analyst estimates of $7.96 – it was the outlook that was less than promising). I have a feeling that HollyFrontier may follow this same trend – great returns for 3Q2013, but negative forward-looking prospects. The second example is stock in Sprint Corporation. The earnings report came in worse than expected based on subscriber losses throughout 3Q2013, but a positive outlook going forward. This has propelled the stock from $6.70 before its 3Q3013 earnings release on October 30th to $7.20 today (a 7.24% increase). It’s also important to note that put option volume in the week before its earnings release was over 3 times call option volume.

Summary

I certainly wouldn’t rule out HollyFrontier as a long-term acquisition, but I definitely wouldn’t use high call option volume as a core reasoning for purchasing stock in the company ahead of an earnings report. The stock has seen virtually no net price change from the beginning of the year (-0.11%), while its PE and PS ratios have stayed mostly stable as well. Two of HollyFrontier’s competitors underperformed analyst EPS estimates for 3Q2013 (Phillips 66 was 7.4% lower than expected and Western Refining, Inc. was 35.3% lower than expected). None of the companies mentioned in the charts below increased more than 4% since the earnings release (Valero Energy Corporation increased less than 1% after its EPS for 3Q2013 came in 39% higher than analysts’ expectations.

Recommendation

I cannot make a recommendation on the short-term trading prospects of HollyFrontier. There are multiple analysts who follow these stocks on a daily basis and are still only right 50% of the time on quarterly earnings. However, with an impressive earnings yield (18.8%), FCF yield (19.32%), book to market ratio (0.7321), dividend yield (2.58%), and reasonable PS ratio (0.4204), this is a reasonable value pick that will perform as a long-term holding.

Two things I would like to point out before I get too in-depth with this analysis. First of all, one of the most important inputs in the profitability of oil refiners is the price of oil. As you can see from Figure 1, the price of oil during July 2013 to September 2013 (the quarter the company is reporting for) is the highest it has been all year. This is certainly a good sign for HollyFrontier, as its profitability has fallen behind its peers in recent quarters. Companies with shrinking margins tend to trade at higher price-to-sales ratios and lower price-to-earnings ratios than those of their peers. This is reflected in the PE ratio of oil refiners, where HollyFrontier has the lowest ratio versus its peers (showing an underpricing in the company’s stock – see Figure 2), and is also reflected in the PS ratio, where HollyFrontier has the highest PS ratio versus its peers (showing an overpricing in the company’s stock – see Figure 3). The downside to the company is that investors take into account the present value of all future cash flows when pricing a stock, and the price of crude oil has fell from over $110 per barrel in September to $93.39 today – not a good sign for the company’s bottom line for the 4Q2013 reporting.

Do Not Let Speculative Option Traders Deceive You

The second perspective that is important to mention is, historically, high option volume (whether it is puts or calls) does not indicate direction of a stock following its earnings report. Two recent examples were Apple, Inc.’s quarterly earnings released last week that were preceded by high call option volume. Before the report, the stock was trading at $529.88 versus $526.85 (keep in mind that the actual EPS of $8.26 was higher than analyst estimates of $7.96 – it was the outlook that was less than promising). I have a feeling that HollyFrontier may follow this same trend – great returns for 3Q2013, but negative forward-looking prospects. The second example is stock in Sprint Corporation. The earnings report came in worse than expected based on subscriber losses throughout 3Q2013, but a positive outlook going forward. This has propelled the stock from $6.70 before its 3Q3013 earnings release on October 30th to $7.20 today (a 7.24% increase). It’s also important to note that put option volume in the week before its earnings release was over 3 times call option volume.

Summary

I certainly wouldn’t rule out HollyFrontier as a long-term acquisition, but I definitely wouldn’t use high call option volume as a core reasoning for purchasing stock in the company ahead of an earnings report. The stock has seen virtually no net price change from the beginning of the year (-0.11%), while its PE and PS ratios have stayed mostly stable as well. Two of HollyFrontier’s competitors underperformed analyst EPS estimates for 3Q2013 (Phillips 66 was 7.4% lower than expected and Western Refining, Inc. was 35.3% lower than expected). None of the companies mentioned in the charts below increased more than 4% since the earnings release (Valero Energy Corporation increased less than 1% after its EPS for 3Q2013 came in 39% higher than analysts’ expectations.

Recommendation

I cannot make a recommendation on the short-term trading prospects of HollyFrontier. There are multiple analysts who follow these stocks on a daily basis and are still only right 50% of the time on quarterly earnings. However, with an impressive earnings yield (18.8%), FCF yield (19.32%), book to market ratio (0.7321), dividend yield (2.58%), and reasonable PS ratio (0.4204), this is a reasonable value pick that will perform as a long-term holding.

Figure 1 – YTD Crude Oil Spot Price

Figure 2 – YTD PE Ratio of Comparable Oil Refiners

Figure 3 – YTD PS Ratio of Comparable Oil Refiners

RSS Feed

RSS Feed