The Federal Reserve Bank

"Can you make some recommendations on municipal bond funds? I like municipals due to their exemptions from federal capital gains tax. What are things I should consider when looking for a fund?"

I want to first apologize if I am repeating things that you already know. I try to explain things as clearly and concisely as possible, but I know that it doesn’t always happen that way. I am going to first cover current trends in the bond market (by briefly covering fed monetary policy) then move more towards municipal bonds before recommending the best funds based on the current state of the market. A little disclaimer before we get started – I am writing this from the perspective that you are already interested in buying a municipal bond fund, but need to decide which one exactly to buy. I am not personally invested in any bond funds as I like to know everything I can possibly know about what my money is invested in. Personally, I find bonds to be among the most boring things on the face of the earth and therefore cannot bring myself to do extensive research on the funds. If I end a week losing money (as I did the first week of the government shutdown), I literally will spend hours researching what I did wrong and changing my investment strategy based on the newest events. Okay, now I’m just rambling… now onto the bond market:

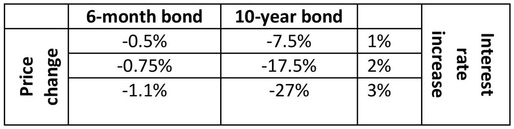

I am going to first start with explaining the possible implications for bond prices on rising rates. This applies to the bond market as a whole, not just municipals. There are essentially two things that change when interest rates are artificially raised or lowered by the fed (dubbed “quantitative easing” or “QE” by the media). When the fed purchases treasuries and mortgage backed securities (as they are doing now at a rate of $85 billion per month), interest rates go down. This is part one of the equation on a macro level – interest rates. Lowering the interest rates on public and private debt causes the prices – part two of the equation – to rise. This is because people begin to pay more for the “old bonds” that are paying 5% coupons as opposed to the “new bonds” that are only paying a 2% coupon. The opposite of this is also true; and unfortunately where we are moving towards as the fed contemplates ending their QE program. That is, the “old bonds” that have gone up drastically in value will start to lose their value as the “new bonds” start paying higher coupon rates. Therefore, in a falling rates environment, bond funds generally perform. And in a rising rates environment, bond funds perform poorly. This part of macro bond funds, or what they refer to as “interest rate risk”, is pretty intuitive. What is not intuitive is when or how the fed will start to cause these rates to rise. Therefore, you need to choose a bond fund that has the lowest interest rate risk.

To illustrate the interest rate effect of bond prices, I will use two different examples at opposite ends of the spectrum. The first is a 6-month bond and the second is a 10-year bond. Because the implications for holding a 6-month bond in a rising-rate environment are much less than that of holding a 10-year bond in a rising rate environment, there are massive differences in the price changes of funds holding these different bonds. Put simply, a fund holding a 6-month bond will probably just suck it up and hold the bond until expiration instead of selling it in favor of a bond with a higher coupon. Conversely, a fund holding 10-year bonds will want to get rid of them as quickly as possible because they don’t want to be making 3% for the next 10 years when the rest of the market is making 5%. The following are rough estimates for price changes of a 6-month bond and 10-year bond based on interest rate increases of 1%, 2%, and 3%. Note that these are not exact estimates and this examples ignores the impact of convexity. It also assumes that there is a simultaneous change in interest rates across the bond yield curve:

I am going to first start with explaining the possible implications for bond prices on rising rates. This applies to the bond market as a whole, not just municipals. There are essentially two things that change when interest rates are artificially raised or lowered by the fed (dubbed “quantitative easing” or “QE” by the media). When the fed purchases treasuries and mortgage backed securities (as they are doing now at a rate of $85 billion per month), interest rates go down. This is part one of the equation on a macro level – interest rates. Lowering the interest rates on public and private debt causes the prices – part two of the equation – to rise. This is because people begin to pay more for the “old bonds” that are paying 5% coupons as opposed to the “new bonds” that are only paying a 2% coupon. The opposite of this is also true; and unfortunately where we are moving towards as the fed contemplates ending their QE program. That is, the “old bonds” that have gone up drastically in value will start to lose their value as the “new bonds” start paying higher coupon rates. Therefore, in a falling rates environment, bond funds generally perform. And in a rising rates environment, bond funds perform poorly. This part of macro bond funds, or what they refer to as “interest rate risk”, is pretty intuitive. What is not intuitive is when or how the fed will start to cause these rates to rise. Therefore, you need to choose a bond fund that has the lowest interest rate risk.

To illustrate the interest rate effect of bond prices, I will use two different examples at opposite ends of the spectrum. The first is a 6-month bond and the second is a 10-year bond. Because the implications for holding a 6-month bond in a rising-rate environment are much less than that of holding a 10-year bond in a rising rate environment, there are massive differences in the price changes of funds holding these different bonds. Put simply, a fund holding a 6-month bond will probably just suck it up and hold the bond until expiration instead of selling it in favor of a bond with a higher coupon. Conversely, a fund holding 10-year bonds will want to get rid of them as quickly as possible because they don’t want to be making 3% for the next 10 years when the rest of the market is making 5%. The following are rough estimates for price changes of a 6-month bond and 10-year bond based on interest rate increases of 1%, 2%, and 3%. Note that these are not exact estimates and this examples ignores the impact of convexity. It also assumes that there is a simultaneous change in interest rates across the bond yield curve:

Although these are rough mathematical estimates based on historical bond sensitivity to the fed funds rate, you can see the massive difference in price change of 6-month bonds versus 10-year bonds. Because of this, I can only recommend what they refer to as “ultrashort bond funds”. These funds’ holdings generally have maturity dates of 3-months to 1-year, resulting in a low level of interest-rate risk. In the ‘90s, these funds were literally used as cash alternatives at some brokerage firms because of how safe managers thought they were. Unfortunately, right before the recent financial crisis, most of their holdings were in mortgage-backed securities (worst thing to be holding during a mortgage crisis with falling homes prices). Although these funds performed VERY poorly during the financial crisis, it is my belief that the managers learned their lesson, and they are relatively low-risk investments today.

Now moving on to recommendations. Because I now only use TD Ameritrade for both my options-trading and [stock] investing accounts, I can only research funds that are sold through their brokerage. I would guess that there is a lot of overlap between TD Ameritrade and other brokerages, but I just wanted to point out that some of the funds I mention will not be available at other sites, and vice-versa.

Now moving on to recommendations. Because I now only use TD Ameritrade for both my options-trading and [stock] investing accounts, I can only research funds that are sold through their brokerage. I would guess that there is a lot of overlap between TD Ameritrade and other brokerages, but I just wanted to point out that some of the funds I mention will not be available at other sites, and vice-versa.

As you can see, these funds have very low returns compared to stocks and relatively low returns compared to other bond funds. It is hard to swallow earning 2% per year on a bond fund when the S&P 500 is up over 19% YTD with almost everyone saying there is nowhere to go but up. However, this run cannot last forever, and your best bet for making money in an uncertain market with dovish fed chairwoman (Janet Yellen) is in short-term municipal funds (if municipal bonds are something you are still interested in). Let me know if ultrashort muni funds aren’t what you are looking for and perhaps I can make different recommendations.

RSS Feed

RSS Feed