"What are your thoughts on Tesla Motors? The company's newest sedan recently received a perfect crash-test rating from Consumer Reports, and their sales have skyrocketed."

1. Chrysler vs. Tesla – Market Capitalization and Sales

The Wall Street Journal reported Monday that Chrysler is filing for an IPO. The UAW Heath Trust currently owns 41.5% of the company, with the remaining share owned by Italian car maker Fiat S.p.A. The issue at hand is that Fiat wants to purchase the share of Chrysler that it does not already own. However, UAW believes their share is worth $4.27 billion while Fiat believes UAW’s share is worth $1.75 billion. While the most viable figure is most likely somewhere in the middle, this gives Chrysler a valuation somewhere in between $4.2 billion (based on Fiat’s measurements) and $10.3 billion (based on UAW’s measurements). In the 12 months ended in June, Chrysler sold 2.3 million vehicles, compared to about 20,000 that Tesla produces in a year. Tesla’s biggest bulls estimate that the company can sell 400,000 vehicles per year by year 2025. Now I understand that a lot can change in the next 13 years, but Tesla is currently valued at $22 billion (between 2.14x and 5.24x Chrysler’s current valuation).

2. Tesla’s Emerging Competition

The Wall Street Journal reported on September 16th that General Motors (GM) is developing an electric car that can go 200 miles on a charge for around $30,000. This would be a huge hit to Tesla as their 3 major competitive advantages are: 1. Relatively low cost of electric vehicles, 2. Sportiness of electric vehicles, and 3. Safety of electric vehicles. GM’s new electric vehicle (ETA TBA) would easily beat Tesla in the price category (estimated $30,000 vs. $63,570 with Federal Tax Credit). The sportiness will be Tesla’s biggest competitive advantage, but faces upcoming product releases from BMW and Mercedes-Benz – both companies that are known to produce high-performance luxury vehicles. Lastly, the safety benefits of the Tesla Model S are a result of the car being a fully electric vehicle as opposed to technical/mechanical inventions on Tesla’s part. As a result of not needing a gasoline engine or advanced multi-gear drivetrain, electric cars have much more space for crumple zones and other safety features.

3. Not a Level Playing Field (but soon will be with emerging competition)

As mentioned briefly in part (2), Tesla’s sales are partly fueled by tax subsidies (a benefit that larger car manufacturers will soon be able to enjoy). This provides a $7,500 tax credit to anyone who purchases a zero emission vehicle. In California, where most of Tesla’s cars are sold, the government provides an even larger $12,500 tax credit.

4. Misleading Metrics

Tesla recently reported a 33,571% increase in California car sales, causing a more than threefold increase in Tesla’s stock price in less than 3 months. This information, in conjunction with revenue growth, was reported in Tesla’s 1Q13 earnings report and 2Q13 earnings report (released 05/08/2013 and 08/07/2013, respectively). These last two periods reported revenue quarterly YoY growth of 5,542.615% and 4,446.853%, respectively. These two figures are the main driving forces behind the massive stock price increase this year. Now let me tell you why they are EXTREMELY misleading: they didn’t even sell a car that was priced below $100,000 until less than a year ago! They went from specialty (think Ferrari or Lamborghini) to mainstream electric – of course their reported revenue quarterly YoY growth is going to skyrocket during that transition.

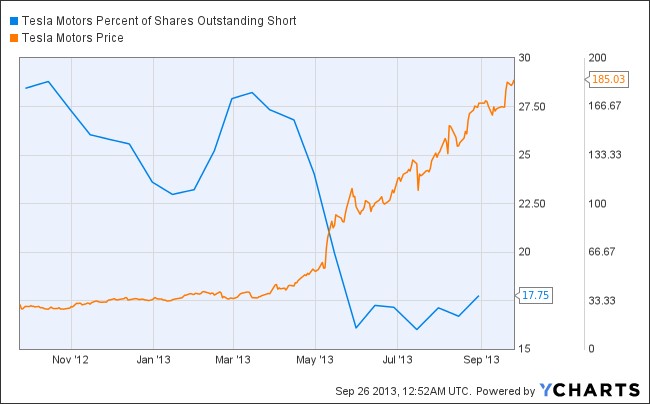

5. A Short Squeeze Has Caused Massive Technical Momentum (see figure 3)

Conclusion

Great company. Good candidate for short term traders/speculators. Bad candidate for long-term investors.

Sources: WSJ (where indicated), yCharts (fig. 1,2,3)

The Wall Street Journal reported Monday that Chrysler is filing for an IPO. The UAW Heath Trust currently owns 41.5% of the company, with the remaining share owned by Italian car maker Fiat S.p.A. The issue at hand is that Fiat wants to purchase the share of Chrysler that it does not already own. However, UAW believes their share is worth $4.27 billion while Fiat believes UAW’s share is worth $1.75 billion. While the most viable figure is most likely somewhere in the middle, this gives Chrysler a valuation somewhere in between $4.2 billion (based on Fiat’s measurements) and $10.3 billion (based on UAW’s measurements). In the 12 months ended in June, Chrysler sold 2.3 million vehicles, compared to about 20,000 that Tesla produces in a year. Tesla’s biggest bulls estimate that the company can sell 400,000 vehicles per year by year 2025. Now I understand that a lot can change in the next 13 years, but Tesla is currently valued at $22 billion (between 2.14x and 5.24x Chrysler’s current valuation).

2. Tesla’s Emerging Competition

The Wall Street Journal reported on September 16th that General Motors (GM) is developing an electric car that can go 200 miles on a charge for around $30,000. This would be a huge hit to Tesla as their 3 major competitive advantages are: 1. Relatively low cost of electric vehicles, 2. Sportiness of electric vehicles, and 3. Safety of electric vehicles. GM’s new electric vehicle (ETA TBA) would easily beat Tesla in the price category (estimated $30,000 vs. $63,570 with Federal Tax Credit). The sportiness will be Tesla’s biggest competitive advantage, but faces upcoming product releases from BMW and Mercedes-Benz – both companies that are known to produce high-performance luxury vehicles. Lastly, the safety benefits of the Tesla Model S are a result of the car being a fully electric vehicle as opposed to technical/mechanical inventions on Tesla’s part. As a result of not needing a gasoline engine or advanced multi-gear drivetrain, electric cars have much more space for crumple zones and other safety features.

3. Not a Level Playing Field (but soon will be with emerging competition)

As mentioned briefly in part (2), Tesla’s sales are partly fueled by tax subsidies (a benefit that larger car manufacturers will soon be able to enjoy). This provides a $7,500 tax credit to anyone who purchases a zero emission vehicle. In California, where most of Tesla’s cars are sold, the government provides an even larger $12,500 tax credit.

4. Misleading Metrics

Tesla recently reported a 33,571% increase in California car sales, causing a more than threefold increase in Tesla’s stock price in less than 3 months. This information, in conjunction with revenue growth, was reported in Tesla’s 1Q13 earnings report and 2Q13 earnings report (released 05/08/2013 and 08/07/2013, respectively). These last two periods reported revenue quarterly YoY growth of 5,542.615% and 4,446.853%, respectively. These two figures are the main driving forces behind the massive stock price increase this year. Now let me tell you why they are EXTREMELY misleading: they didn’t even sell a car that was priced below $100,000 until less than a year ago! They went from specialty (think Ferrari or Lamborghini) to mainstream electric – of course their reported revenue quarterly YoY growth is going to skyrocket during that transition.

5. A Short Squeeze Has Caused Massive Technical Momentum (see figure 3)

Conclusion

Great company. Good candidate for short term traders/speculators. Bad candidate for long-term investors.

Sources: WSJ (where indicated), yCharts (fig. 1,2,3)

Figure 1 - Market Capitalization of Tesla, GM, and Ford

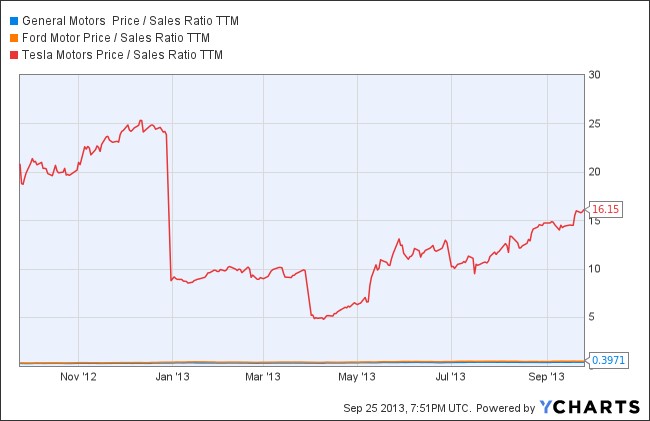

Figure 2 - Price-to-Sales ratios of Tesla, GM, and Ford

Figure 3 - Short Float vs Price of Tesla As you can see from this graph, a short squeeze in Tesla stock began around the beginning of March 2013. This same phenomenon occurred to car manufacturer Volkswagen in 2008 when a short squeeze temporarily drove the shares of the Volkswagen from 210.85 euros to over 1,000 euros in less than two days, briefly making it the most valuable company in the world. This short squeeze has caused massive technical momentum that has driven Tesla's stock price to an unsustainable valuation.

RSS Feed

RSS Feed